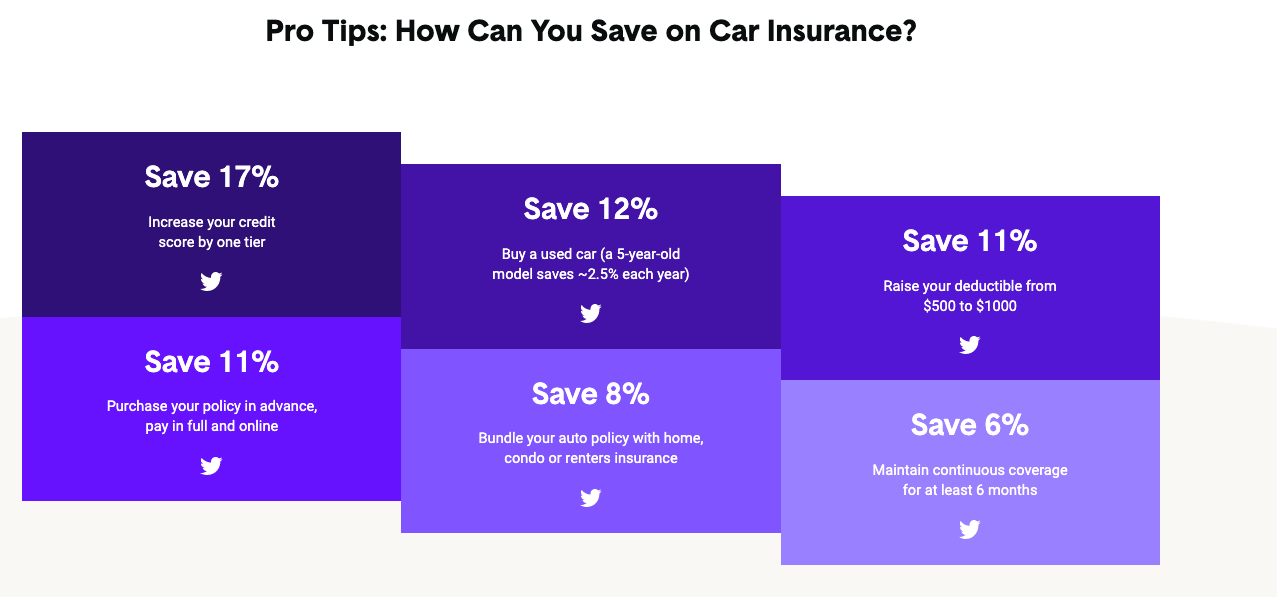

Question of the Day: What can save you the most when it comes to auto insurance: 1) Improving credit score 2) Driving a used car 3) Paying for policy in advance?

Answer: Improve credit score by one tier can reduce auto insurance rates by 17%

Questions:

- Why do you think that having a higher credit score (a measure of how you manage credit) would lower your car insurance rates?

- Used cars also can help you save on your car insurance. Why do you think insurance companies give you a discount if you drive a used car?

- If the average auto insurance policy is $1,502 (much higher for young adults), how much could you save (in $) if you raised your credit score a tier, drove a 5-year old used car AND paid your premium in advance?

Behind the numbers (Zebra):

---------------

Pair these NGPF resources with this QoD:

About the Author

Tim Ranzetta

Tim's saving habits started at seven when a neighbor with a broken hip gave him a dog walking job. Her recovery, which took almost a year, resulted in Tim getting to know the bank tellers quite well (and accumulating a savings account balance of over $300!). His recent entrepreneurial adventures have included driving a shredding truck, analyzing executive compensation packages for Fortune 500 companies and helping families make better college financing decisions. After volunteering in 2010 to create and teach a personal finance program at Eastside College Prep in East Palo Alto, Tim saw firsthand the impact of an engaging and activity-based curriculum, which inspired him to start a new non-profit, Next Gen Personal Finance.

SEARCH FOR CONTENT

Subscribe to the blog

Join the more than 11,000 teachers who get the NGPF daily blog delivered to their inbox:

MOST POPULAR POSTS